Thank NZ for strong export lamb demand

We recently had a query as to whether there was much seasonality in New Zealand lamb slaughter. We have covered this before, but given New Zealand are our only major competitor in lamb export markets, it’s worth another look.

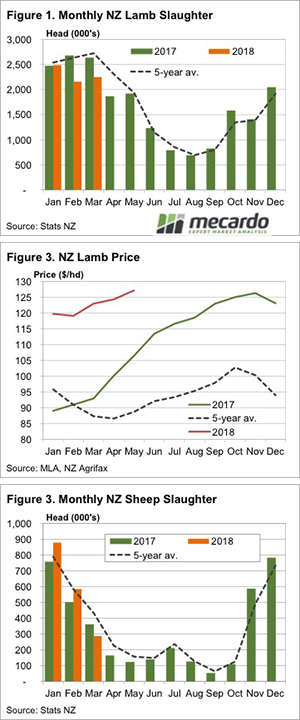

Australian lamb slaughter has some seasonality, with the five year average low month, July, coming in 18% lower than the peak in October. In New Zealand they have real seasonality. The lowest slaughter month of August is 75% lower than the peak in March. That is, a quarter the number of lambs are slaughtered in August, than are slaughtered in March.

Figure 1 shows that January to March slaughter is usually very strong. To put NZ into perspective, their January to March slaughter averages over 2.5 million head. Australia’s highest slaughter month on record in 2.2 million head.

As well as illustrating annual seasonality, figure 1 gives us some idea as to why export demand for lamb has been strong this summer and autumn. The falling NZ sheep flock and lamb crop has seen a heavy fall in lamb slaughter. While January slaughter was similar to last year, February and March were down 19 and 14% respectively.

Lower lamb supply out of New Zealand simply means that prices are going to be higher there, which can see demand shift to Australia. Heavy Australian slaughter has helped fill the hole left by New Zealand.

Lower slaughter has seen record lamb prices in New Zealand. Figure 2 shows lamb prices for 17.5 kgs cwt lambs in NZ has been rising to record levels at a time of year when they normally hit their seasonal lows. Over the first five months of 2018 lamb prices have averaged 24% higher than 2017.

Sheep slaughter shows similar, but more pronounced seasonality in New Zealand. Figure 3 shows monthly sheep slaughter. The peak month of January is eight times larger than the lows of September.

What does it mean/next week?:

It seems whenever we look at New Zealand sheep and lamb its positive for our market. In the short term we can expect export demand for Australian lamb to remain strong as New Zealand slaughter enters its seasonal decline.

Lower lamb slaughter this year might indicate the start of a flock rebuild, which in the medium term is negative for export demand. Sheep slaughter has been stronger, which might will put a dampener of the flock rebuild, especially as there were supposedly fewer lambs born last year.