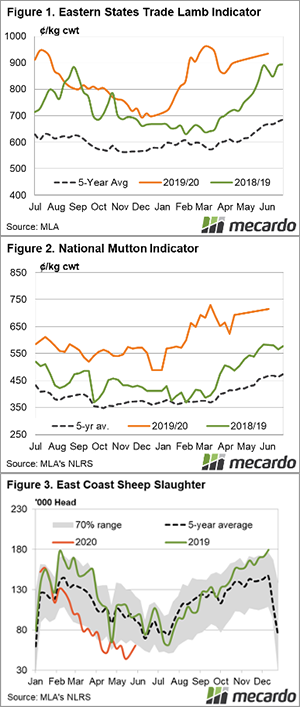

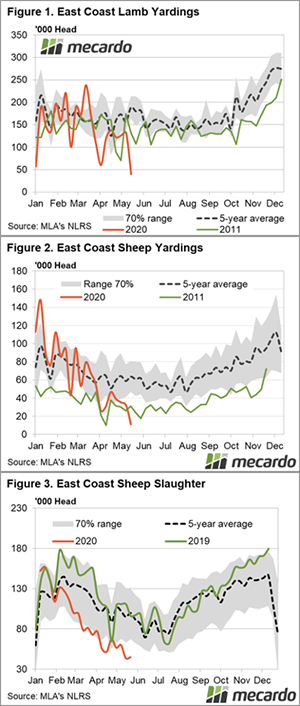

Prices for most sheep and lamb categories took a turn south this week as resistance was found at recent levels. That was despite lower yardings; marking the entry into the tight winter for sheep and lamb supply.

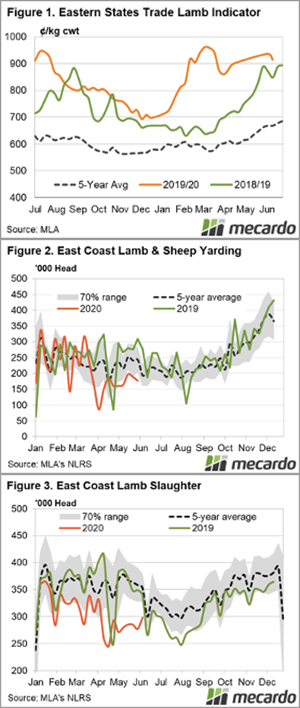

Saleyard prices for most categories declined week on week. The Eastern States Trade Lamb Indicator (ESTLI) fell 2.4% to 914¢/kg cwt (Figure 1), but what was lost in the East was made up in the West. Trade lambs in Western Australia gained 2.3% to 804¢/kg cwt.

East coast restocker lambs didn’t get the support they’ve enjoyed of late, falling slightly to 961¢/kg cwt. It was light lambs that took the hardest hit though, losing 32 cents or 3.5%.

Mutton prices lost ground as well. The National Mutton indicator shed 2.7% or 18 cents to 659¢/kg cwt.

Last week saw fewer lambs and sheep running through eastern saleyards again. Lamb yardings were down 4%, and sheep yardings down 2% to see a combined 177,365 head yarded (Figure 2). Victoria drove much of the decline in lamb throughput, with nearly 10,000 fewer head yarded.

East coast lamb slaughter has been tracking well below the five year average since February. However, an 8% lift last week saw lamb slaughter was just shy of the five year average seasonal low (Figure 3). On the other hand, sheep slaughter is currently tracking 31% under the five year average.

Next week:

We’ve entered the official winter lull period for lamb and sheep supply and while there have already been weeks of very low slaughter, tight can get tighter. The Winter rainfall forecast has been changeable to say the least, switching again from average to above-average rainfall for most sheep regions. Let’s hope the current forecast sticks.