Demand & supply heading for a mismatch

Key Points

With harvest underway in parts of the US, the World Agricultural Supply & Demand Estimates (WASDE) report was released last night our time and was met with a neutral response from commentators.

Markets confirmed no surprises with a stable response, with the USDA lifting wheat production by around 1% on the back of stronger South American production. They noted this was slightly more bearish for wheat price outlook.

The expected record US corn crop is combining with other feed grains to look likely to produce a record feed grain crop. The USDA predicting a 5% increase on last year. While the US corn crop is driving 80% of this increase, Mexico, Brazil & Ukraine will also contribute.

This comes at a time when global feed demand has taken a hit with the African Swine Fever wiping out around 70 mill tonne of demand. Adding to this, CV-19 restrictions are impacting gasoline demand, particularly in the US where corn-based ethanol is mandated into the mix.

The upshot is that low prices are expected to continue into next year, with countries who have had their currency devalue against the USD less impacted. This will likely maintain high levels of plantings in these countries despite the lower prices.

Domestically ABARES has lifted the outlook for wheat by 25% from last month, aiming now at a wheat crop of 26.7 mill tonnes, while barley is expected to be up 17% year on year to 10.6 mill tonnes.

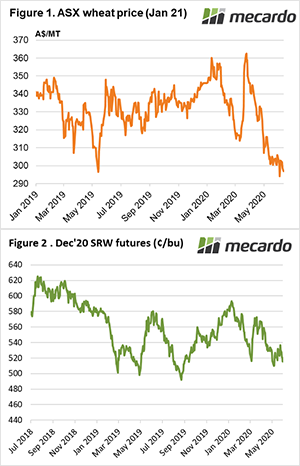

All this positive news for production is weighing on prices, with the ASX Jan 2021 contract easing below the $300 mark to $297, while the US CME Dec 2020 contract after testing the 535-cent mark also pulled back 20 cents per bushel to 515 cents.

Domestic delivered prices continued to ease as we move closer to “new crop” pricing and buyers’ seemingly content anticipating a significant export surplus for the coming harvest. Despite the BOM changing their prediction of median rainfall for the winter, many grain regions are comfortable for now with soil moisture levels, and with forecast showers in the week ahead, are daring to feel optimistic about production.

Next week?

The widespread frosts across eastern Australia continued making the prospect of some (any?) rain slightly more urgent.

I am regularly reminded by experienced grain producers that “it’s not in the bin until it’s in the bin”, however, the prospect for a large crop is in place, with a couple of key rain events needed in late winter and spring to create a year to remember.