Dry continues to see prices trend sideways

The Bureau of Meteorology (BOM) released their three-monthly rainfall outlook yesterday and it provided limited optimism for cattle prices to the end of Winter. The dry June across NSW and southern Queensland is not helping much either with elevated supply here keeping a lid on prices this week.

Being Western Victorian based we have received reasonably good rain so far this season, unfortunately for NSW, southern Queensland and the western half of South Australia the same cannot be said.

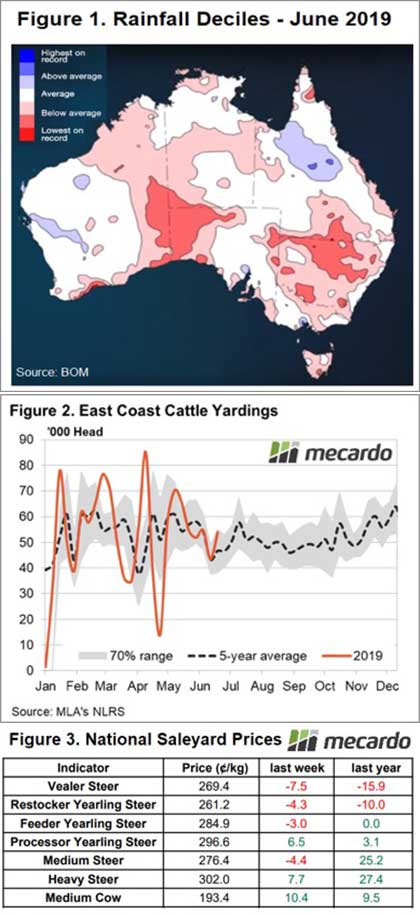

Figure 1 highlights the rainfall deciles for June and it shows large tracts of southern regions across the country suffering under below average rainfall. The prospect isn’t likely to improve as we head toward Spring according to the most recent BOM three month rainfall outlook with drier than average expected for much of the East coast and the southwestern half of WA.

The dry times are keeping East coast cattle yarding levels elevated (Figure 2) and a breakdown across the eastern states shows that it is NSW and Queensland that are contributing most to the higher throughput figures of late.

East coast yardings are trending 15% above the long-term average for this time in the season, this is despite Victorian numbers running below their average trend by 3%. The culprits for the higher East coast throughput levels are NSW and Queensland with yarding levels running 36% and 10% above average, respectively.

The Eastern Young Cattle Indicator (EYCI) reflected the higher east coast supply easing 3.5¢ to close at 488.75¢/kg cwt. Most National cattle price indicators mirrored the EYCI posting declines between 3.0¢ to 7.5¢.

However, processor buyers remaining active chasing the limited stock available to see Processor Yearling Steers, Heavy Steers and Medium Cow lift – Figure 3.

Next week

Reasonable rainfall is expected this week for Victoria and the southwestern coastal tip of WA, but limited falls are slated for the rest of the country. As outlined a few weeks ago, offshore export prices remain firm and this is keeping processor margins running strong, so they will continue to support the market on dips.

However, the extended dry across NSW and Queensland is limiting the opportunity for cattle prices to extend higher. This spells more price consolidation and sideways movement for the short term.