No change to recent stronger trend

AWEX report a market this week that “responded with another week of solid rises”; fine wool continues to be the leader but it was hard to find a category that missed out with an across the board lift in prices. The gap between 18 & 19 microns in Melbourne is now out to 194 cents, this time last year it was +43 cents.

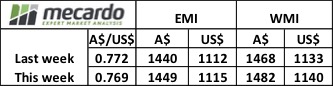

The EMI was up A$0.09, while in US$ terms it improved 3 cents with the Au$ quoted slightly lower for the week. Cardings continue to out-perform, with all 3 selling centres reporting strong increases and the relative Cardings indicators all nudging 1200 cents. (Fig 1.) Note that before 2011 the Cardings indicator rarely bobbed above 600 cents.

The EMI was up A$0.09, while in US$ terms it improved 3 cents with the Au$ quoted slightly lower for the week. Cardings continue to out-perform, with all 3 selling centres reporting strong increases and the relative Cardings indicators all nudging 1200 cents. (Fig 1.) Note that before 2011 the Cardings indicator rarely bobbed above 600 cents.

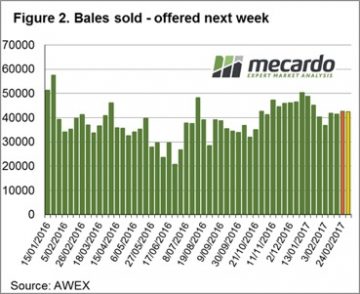

Again, this week 45,000 bales were offered with an increase week-on-week of 1,000 bales sold. Cleared to the trade were 42,500 resulting in a reduced Pass In rate of 4.7%.

Two points regarding clip preparation are worth noting as the wool market dynamics continue to evolve. These points are at the extreme ends of the micron spectrum with change noted in the fine & superfine market as well as the X Bred market.

Two points regarding clip preparation are worth noting as the wool market dynamics continue to evolve. These points are at the extreme ends of the micron spectrum with change noted in the fine & superfine market as well as the X Bred market.

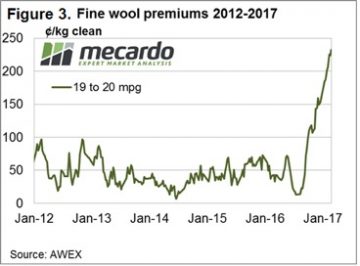

Over recent years while the fine wool premium has hovered at record low levels, there has been little incentive to class out finer lines in the woolshed. These gaps are now starting to open up and classers now should be honing their skills to separate out the finer types aiming to participate in the growing premiums available. (Fig 3).

This week Mecardo noted that the trend to offer unskirted fleece lots had tempered. As the X Bred market has retreated in price the discount for poorly prepared or unskirted wool has increased. This increased concern about preparation is a normal response in a falling market. Both of these opportunities emphasise the need to get good advice from your wool broker when deciding on preparing wool to meet market conditions.

This week Riemann traded solid volumes, with a spread of trades across the 18.5, 19 and 21 MPG types, and for settlements from March 2017 out to July 2018. Price levels were seen as attractive to growers looking to capture some of the market momentum for future clips.

This week Riemann traded solid volumes, with a spread of trades across the 18.5, 19 and 21 MPG types, and for settlements from March 2017 out to July 2018. Price levels were seen as attractive to growers looking to capture some of the market momentum for future clips.

The week ahead

Next week Melbourne reverts to a 2-day sale along with Fremantle and Sydney. The roster is starting to tighten with 42,320 bales listed (42,500 sold this week out of a 45,000-bale offering), and the subsequent weeks have 42 & 40,000 bales listed.

Supply is contracting and demand looks solid so it’s difficult to see any reason for this market to retrace – good times for wool producers ……… about time I can hear some say!