Rising Aussie dollar dampening our grain values

After falling heavily last Thursday night Chicago Soft Red Wheat (CBOT) Futures largely held their ground this week. The real issue for local values came from the Australian dollar, which this week hit a two year high and is dampening the value of our grain.

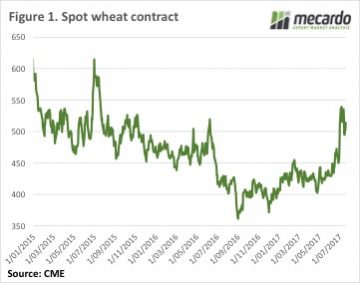

CBOT wheat prices managed to track sideways this week as the market digested the World Agricultural Supply and Demand (WASDE) report and weather outlooks improved. While the spot and Dec-17 CBOT wheat have fallen 50¢ from the peak, the Dec-18 contract is down 35¢. Dec-17 currently sits at 529¢/bu, with Dec-18 at 585¢ and full carry back in the market.

CBOT wheat prices managed to track sideways this week as the market digested the World Agricultural Supply and Demand (WASDE) report and weather outlooks improved. While the spot and Dec-17 CBOT wheat have fallen 50¢ from the peak, the Dec-18 contract is down 35¢. Dec-17 currently sits at 529¢/bu, with Dec-18 at 585¢ and full carry back in the market.

The rise and rise of the Australian dollar has wiped some more value off swap prices. This morning Dec-17 is priced at $242/t and Dec-18 at $268/t. Good employment data yesterday pushed the AUD to 80US¢. The 5¢ rise in AUD since the start of June has wiped $16/t off the value of CBOT wheat futures in our terms.

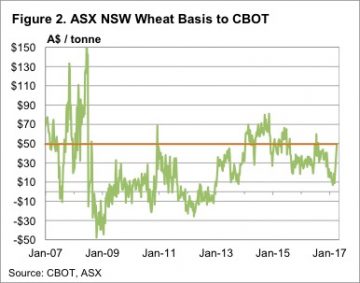

Locally new crop ASX East Coast Jan-18 Wheat futures have also fallen, but basis is strengthening. The Jan-18 ASX contract settled at $290/t yesterday, which at $48 basis is historically pretty strong, but not yet ‘drought’ basis as seen last in 2007 (Figure 2).

After also falling heavily last week, ICE Canola for Jan-18 has steadied at the $515CAD/t level. The Canadian dollar has matched the AUD increases, with the two currencies locked at parity, so swap prices remain around the $515/t value. With local port prices at $530-535/t, the basis value doesn’t look to be there, so swaps would be the way to go at the moment.

After also falling heavily last week, ICE Canola for Jan-18 has steadied at the $515CAD/t level. The Canadian dollar has matched the AUD increases, with the two currencies locked at parity, so swap prices remain around the $515/t value. With local port prices at $530-535/t, the basis value doesn’t look to be there, so swaps would be the way to go at the moment.

The week ahead

The forecast shows another 8 days without rain for anywhere but South West WA and parts of Victoria. The weather is still cool but the need for rain on the East coast is increasing, and basis should continue to climb, for both wheat and canola.

The US market seems to have found a level it’s comfortable with for the time being, but as we move towards the corn and soybean harvest the risk of downside will increase.