Support found at 500¢

Despite rising slaughter rates, and more dry weather, the Eastern Young Cattle Indicator (EYCI) managed to find some support at 500¢. The demand from export markets remains rampant, with slaughter cattle prices hitting new peaks.

Despite rising slaughter rates, and more dry weather, the Eastern Young Cattle Indicator (EYCI) managed to find some support at 500¢. The demand from export markets remains rampant, with slaughter cattle prices hitting new peaks.

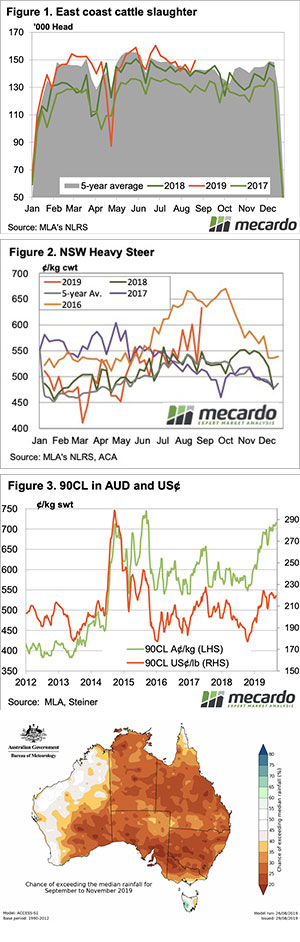

The fall in the EYCI halted this week, with young cattle prices easing 4¢ to stall at 503.75¢/kg cwt. Some of the heavy fall last week can be put down to stronger supply. Figure 1 shows a 6% rise in east coast cattle slaughter, and a 5% lift on the same time last year. The lift in supply was concentrated in Queensland, where a 12% rise for the week carried east coast slaughter higher.

The biggest move we saw in cattle markets this week was the Heavy Steer Indicator in NSW. Figure 2 shows a 108¢ jump on last week, and 33¢ on a fortnight ago, to hit a three year high of 633¢/kg cwt. Heavy Steer in NSW have only been more expensive at this time in 2016, and strong export prices are driving the rise.

Figure 3 shows export prices continue to rise, this week thanks to an increase in the US value. Figure 3 shows how much the lower Aussie dollar has done for export values, and therefore cattle prices. The 90CL price in US terms is at the top of the three year range, but in our terms it is approaching record values. This week’s price of 715¢/kg swt is a new four year high, and just 30¢ off an all time record.

What does it mean/next week?:

The latest Bureau of Meteorology (BOM) three month outlook (figure 4), released yesterday, doesn’t hold a lot of joy for cattle producers. With only parts of WA and Tasmania with a better than 50% change of stronger than median rainfall, it looks like spring might again fail for many.

The forecast doesn’t mean it’s not going to rain, but the chances of good rains are low. This suggests pressure on young cattle, and support for finished cattle is likely to continue for the rest of the year.