Teetering on the edge

It was a big week in the grain markets with the release of crop forecasts from the US and Australia. The market teeters on the edge of a bull market causing a high degree of volatility. In this weeks market comment we take a look at the A$, futures and new crop basis.

It was a big week in the grain markets with the release of crop forecasts from the US and Australia. The market teeters on the edge of a bull market causing a high degree of volatility. In this weeks market comment we take a look at the A$, futures and new crop basis.

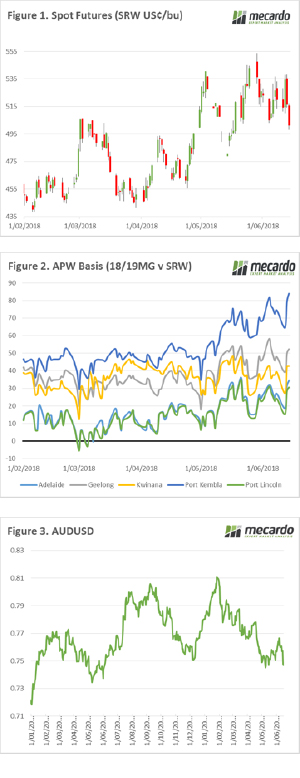

The futures market has been volatile this week (Figure 1), with Chicago spot futures trading in a range of 501.5-534.5¢/bu. The market is currently at $5 below the close on the last Friday. The midweek rally was as a result of the generally bullish data in the WASDE report, especially the sudden fall in Russian production estimates. Gravity, however, had its impact on the market, with traders digesting the WASDE report with concerns related to high ending stocks and uncertainty in the Russian seeding numbers.

Our greatest concern at present for Australian wheat producers and consumers is the conditions locally, especially in NNSW & QLD. In these regions, the crop has gone into minimal soil moisture and received little in the way of meaningful rainfall. The domestic demand in these areas is high and the likely drop in production will be a primary driver of basis on the east coast.

In Figure 2, the new crop basis levels are displayed and we can see the strong increase in levels in the past month as conditions show little sign of improvement. A higher basis level indicates that we should be considering selling physical, however at this point in time, production risk is too high in most places to consider substantial volumes.

The A$ has taken a nose dive in the past day (Figure 3). This was a result of weak Chinese economic and neutral Australian employment data. A lower A$ makes our export commodities more attractive versus competing origins, on the other hand, it makes our inputs more expensive in local terms.

What does it mean/next week?:

The June/July period tends to have a high degree of volatility as the northern hemisphere heads for harvest. This year with supply and demand teetering on the edge of a neutral/bullish market, it will not be unexpected to see large swings in pricing on futures.

The big risk is to the Australian crop and with the BOM forecasting a drier than average 3 month period, we need to take this into account in our marketing plans.